This post is about six (6 ) categories you must understand to build a better credit score for your personal finance. While on my journey to becoming debt-free, I had to start by going beyond the surface and do some heavy and deep reviewing of my personal finances which I will share in this article titled six (6) Categories You Must Understand To Build A Better Credit Score. Before I could begin the process, I had to get educated on understanding the elements that affect my credit.

I had purchased a car, a house, and applied for a credit card, but never in my life have I ever thought about these six (6) categories! Before you apply for your next credit card, car, or house loan, you should understand and know these six (6) categories because I know you will save money and increase your credit score. When I became educated on these six (6) categories, my credit score increased by 65 points. My score is now in the 700 range, but I am trying to get it into the 800 range. The highest you can achieve is 850.

This post is about six (6) categories you must understand to build a better credit score and save money.

Here are the categories, and I will explain them in detail: Payment history, credit card use, derogatory marks, credit age, total accounts, and credit inquiries. You should examine these six (6) categories at least quarterly when reviewing your credit report. You start by going to Credit Karma because it is accessible and easier to understand. Once you are in Credit Karma, click “Overview” at the top of the menu and select “score details.” There are six (6) critical steps you need to know and understand before repairing, applying, and understanding how to maintain good credit.

Scroll down a little and review these six (6) categories in your report.

1. PAYMENT HISTORY

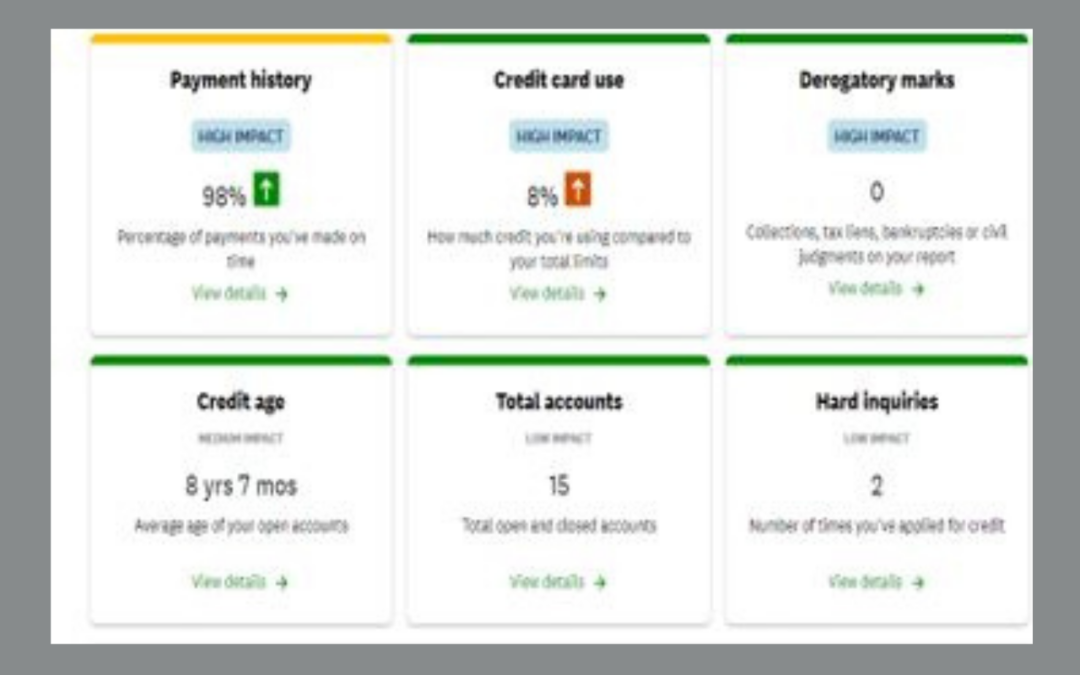

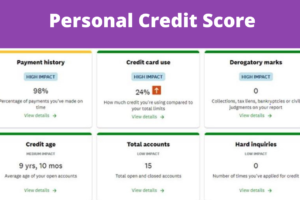

This is created when you pay your bills on time. It makes up 35% of your credit. Although the credit bureaus use these elements to collect data and determine your credit score, everyone’s data will differ. The more payments you miss, the more damaging your credit, reducing your score. Call your lender to make payment arrangements when you cannot meet your obligations.

2. CREDIT CARD USE

You need to make your payments on time, but you also need to watch how you use your credit cards. Credit card use is also known as credit utilization and makes up 30% of your credit. I have two credit cards totaling $10K together, but I only use six percent of my credit cards. Because of my usage in this category, I received an excellent rating. Using too much of your credit card or maxing out your credit card can negatively impact your score.

While you need to establish credit, it does not mean you need to max out your credit cards because you have them. Utilize them wisely. As a young adult, I did not understand this. You should use 30% or less of your credit card, ideally only 10%. You do not need to carry a balance to maintain your credit score. You should make sure your account is active, so it will not closeout. You should pay your balance in full every month when the payment is due. Remember, you must pay this money back! If you have a credit card that gives you points for using it, you can redeem your points for cash or rewards.

3. DEROGATORY MARKS

These marks consist of collections, tax liens, bankruptcies, or civil judgments that could be on your report. Because derogatory marks can significantly impact your credit score, you want to avoid them because they will stay on your account for 7-10 years. If you find wrong information on your credit report, you should dispute it with the credit bureaus.

4. CREDIT AGE/LENGTH

This tells how long you have had each account has been listed on your credit report, arranging from the oldest to the newest. The length of your credit history accounts for 15%. This shows how long you had credit and how responsible you are for handling credit. Some who are new or trying to establish credit could be considered a risk to a lender because they have no viable credit history yet. In this category, this only happens as time passes.

According to Credit Karma, here are three things about your credit age you should know:

- Do not close your oldest credit card; it is what gives you long credit history.

- Sometimes creditors will close credit card accounts because of non-use. The use of an old card periodically could prevent a potential score drop.

- When an older account (like a mortgage or student loan) falls off your report, your score could drop since you are losing the credit history that comes with that account.

This is good guidance for those who already have an established credit history to keep in mind. To find ways to start building your file and increase your credit score, I recommend reading “Get Good with Money” by Tiffany Aliche. It is an excellent book that will also guide you on getting your personal finances in order!

5. TOTAL ACCOUNTS/ CREDIT MIX

Total accounts/credit mix makes up 10%. This category tells you how accounts are opened and closed. It also shows types of accounts, revolving credit, and installment credit. These are credit mixes! Having a different credit mix, such as credit cards and loans, will help your credit. Although having a good number and a mixture of other accounts, it is still not as crucial as using credit responsibly. Your accounts will grow over time.

6. CREDIT INQUIRIES (Hard and Soft)

When applying for credit, whether a credit card, a personal loan or renting an apartment, the company will do a credit check. This is called a credit inquiry which accounts for 10%. There are two types of credit inquiries soft and hard:

Soft Credit Inquiries do not significantly have a profound impact on your credit. These inquiries are done by creditors and do not require your permission, which gives a brief overview of your credit behavior but not in full detail. For example, when you see those “pre-approved” letters come in your mailbox saying you are approved for this credit card. This is an estimated guess because they do not have all the details. It is also defined as a soft inquiry when you pull your credit.

Hard Credit Inquiries are more detailed because it requires your permission. They need your social security number, and this can impact your score. Usually, a bank or car dealer makes hard credit inquiries with your consent.

Even though these inquiries are temporary, and you can recover within three months, they can stay on your credit report for up to two years. You should plan and minimize your hard inquiries to 9-12 months before trying to get a mortgage or big a loan.

Out of these six (6)categories, the accounts that are highly impacted are payment history and credit cards because they account for 65% of your total score; therefore, you should always pay your bills on time, and when you cannot call and plan a strategy for paying your creditors. Use no more than 30% or less when using your credit cards.

Besides understanding these six (6) Categories to Build A Better Credit Score and Save Money, there are other elements, such as salary and how long you have been on the job; lenders consider that when you apply for personal loans. These elements help the lenders determine your creditworthiness to make a wise and accurate decision.

Credit Karma is a good starting point to understanding and repairing your credit. These categories also reveal your money behaviors!

Try extremely hard to stay out of the red zone. You will see all green and one yellow in the illustrated graphic, which is good. I received a yellow because I was late with a payment twice. Also depicted in this illustration, the “credit card use” category also gives me a warning sign that I am using too much on my credit card(s).

Because of the teaching about credit repair from Brittany Greene, the owner of Crowned Financials, LLC, my credit score increased by 65 points. I highly recommend her book “A to Z Credit.” I like this book because it is short, informative, and gives a synopsis of how you, too, can increase your credit score.

This post is all about six (6) categories you must understand to build a better credit score and save money.

Please share if you know someone else who could benefit from the post.

Other Post(s) and Resource(s) You May Like:

“A TO Z CREDIT” BRITTANY GREENE

Recent Comments