This post is all about 30 Financial Management Questions You Should Ask Yourself! This is a financial management questionnaire survey based on a small sample done through Facebook. Although this is a 30-day survey done by Facebook family, friends, & new friends, it provides a glimpse of our financial status and how well we manage our money. The survey contains 30 related financial questions that consisted of yes or no, multiple choices, and short answer questions.

DO YOU KNOW YOUR CREDIT SCORE?

Out of all the respondents that participated in this small survey only two people did not know their credit score

DO YOU HAVE A BUDGET?

Out of the 11 participants who participated in the short survey, three of them did not have a budget. At one time, I did not have a budget either, however, it is critical that you have a budget because there are a few things it does for you:

- Creates financial stability,

- Track your expenditures,

- Allows you to plan for short or long-term expenses

- Save for major purchases

- Save for unexpected emergencies

- Understand how much cashflow you have, to work with once all expenses are paid

- Keeps you on track and organized

- Helps you control your spending

DO YOU EVER GO OVER YOUR BUDGET?

DO YOU KNOW YOUR CHECKING ACCOUNT BALANCE?

Out of 11 respondents, three respondents did not know their checking account balance.

DO YOU HAVE A CHECKING ACCOUNT?

All 18 respondents said yes. Keep in mind when getting a checking account, you should consider getting a checking and savings account with a local credit union because many of them do not require you to keep a minimum balance

According to the FDIC, it is” estimated 5.4 percent of U.S. households (approximately 7.1 million) were “unbanked” in 2019, meaning that no one in the household had a checking or savings account at a bank or credit union (i.e., bank). Conversely, 94.6 percent of U.S. households (approximately 124.2 million) were “banked” in 2019, meaning that at least one member of the household had a checking or savings account.”

IS YOUR CREDIT SCORE BAD, FAIR, GOOD, VERY GOOD, OR EXCELLENT?

Credit Score range:

- 300-579 = Poor

- 580-669 = Fair

- 670-739 = Good

- 740-799 = Very Good

- 800-850 = Excellent

DO YOU KNOW YOUR CREDIT SCORE NUMBER?

Four (4) out of five (5) said “yes”

DO YOU KNOW THE 5 (five) CATEGORIES THAT MAKE UP YOUR CREDIT SCORE

Payment history (35%) and credit card use (30%), these two categories make up 65% of your credit score. Although there are only five (5) categories that account for your credit score, Credit Karma describes six (6). Derogatory remarks are the sixth one. Even though it does not count percentage-wise, it still can have an impact on your credit score

THE FIVE (5) CATEGORIES ARE:

1. Payment History – 35%

2. Credit Card Use – 30%

3. Credit Age or Length – 15%

4. Total Accounts or Credit Mix – 10%

5. Credit Inquiries – 10% (Hard and Soft)

NAME ONE OF THE FIVE (5) CATEGORIES THAT IMPACT YOUR CREDIT SCORE.

Payment history (35%) and credit card use (30%), these two categories make up 65% of your credit score

CAN YOU GET A COPY OF YOUR CREDIT REPORT FOR FREE?

Eleven (11) out of 11 said “yes!” You can get a free copy of your credit report annually from the major three credit bureaus. You should make this an annual goal to get a copy of your credit report because it will help protect your identity.

{RELATED POST: FIVE (5) POPULAR AGENCIES YOU NEED TO KNOW WHEN IT COMES TO YOUR CREDIT SCORE}

ARE YOU A SAVER?

Eight (8) out of eight (8) said “yes”, they are savers

DO YOU INVEST IN YOUR FINANCIAL EDUCATION?

Six (6) out of six (6) said “yes”

In this small sample survey, 100% of the respondents invested in financial education. While this is great to know, we need more people to invest in their personal financial growth. According to the Milken Institute, only 57% of adults in the United States are financially literate. Financial literacy is essential today. Informed consumers will make better decisions, understand why it is important to save, help reduce debt, and avoid being financially stressed.

DO YOU INVEST IN THE STOCK MARKET?

Four (4) said yes & four (4) said “no” – if you have a 401k, Roth, or an IRA, you invest in the stock market.

DO YOU OWE DEBT?

Eight (8) said “yes” and three (3) said “NO” If you make payments on anything, such as a car or mortgage, you owe debt. This goes back to knowing your four (4) numbers.

DO YOU TELL YOUR MONEY WHERE TO GO OR IT TELLS YOU WHERE TO GO?

Seven (7) out of eight (8) of respondents said that they “tell the money where to go.” If you have a budget, and if you are managing it well, more than likely, you are “telling your money where to go,” instead of it telling you.

DO YOU LEVERAGE DEBT?

Most respondents said “no” that they do not leverage debt. Leveraging debt can be good or bad. It depends on how you use it, requires discipline, and education. Investopedia defines “leverage” as using borrowed money to increase your return on investments.

DO YOU THINK YOU MANAGE YOUR MONEY WELL?

Most of the respondents said “sometimes,” and sometimes we do get off track. Nevertheless, we still need to manage our money and get back on track when we get off track.

DID YOUR PARENTS TEACH YOU HOW TO MANAGE YOUR MONEY?

Six (6) said “No” and one (1) “yes”— Growing up in the 80s money management was never taught in my household. If you received it, you are one of the blessed ones.

DO YOU THINK FINANCIAL MANAGEMENT SHOULD BE MANDATORY IN MIDDLE & HIGH SCHOOL?

100% of respondents agreed that financial management or personal finance should be mandatory for middle and high school students. Presently, there are at least eight (8) states that have a mandatory Financial Management Course for high school students. It should not be an elective but mandatory.

DO YOU THINK WE SHOULD TEACH OUR KIDS HOW TO BUDGET?

Seven (7) out of seven (7) said “yes”

Based on this small survey, 100% of the respondents agreed that we should teach our kids how to budget. Although many would agree that we need to teach our kids about savings and budgeting, how can they teach them? if they have never been taught how, themselves.

It is never too late to learn. We must teach them, so they can avoid less financial stress at an early age.

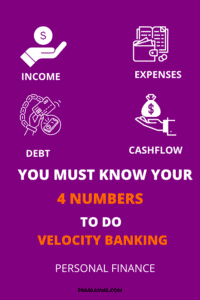

DO YOU KNOW YOUR FOUR FINANCIAL NUMBERS?

These are your FOUR financial numbers:

- Income

- Expense

- Debt

- Cashflow

WHAT IS THE HIGHEST CREDIT SCORE SOMEONE CAN GET 650, 750, 850, OR 950?

Although I knew the highest credit score you can achieve is 850, I purposely selected the wrong one. It is good to know what your credit score is, especially when you are applying for credit.

HAVE YOU EVER LIVED FROM PAYCHECK TO PAYCHECK?

Twelve (12) out 12 responses said they have lived from paycheck to paycheck. WOW! I relate to these respondents. Living from paycheck to paycheck can be very stressful.

NAME ONE FINANCIAL BOOK YOU HAVE READ OR WOULD LIKE TO READ.

I highly recommend you read at least one financial book that will improve your financial status. You can begin with these:

- 21 Day Financial Fast; Michelle Singletary

- How Money Works: Don’t Be A Sucker; Tom Mathews & Steve Siebold

- Get Good With Money; Tiffany Aliche aka the Budgetnista!

- A to Z Credit; Brittany Greene

HAVE YOU EVER HEARD OF THE TERM “VELOCITY BANKING?”

I understand! I had never heard of it until I met a “Financial Geek.” I understand the concept of “velocity banking” originated in Australia.

IF YOU LOSE YOUR JOB TODAY, DO YOU HAVE ENOUGH MONEY TO COVER YOURSELF FOR 30 DAYS?

The majority of respondents said that if they lose their job today, they have enough money to cover them for 30 days. This is an excellent starting point, but our end goal is to have at least six months to a year to cover our living expenses.

DO YOU GIVE MONEY TO YOUR CHURCH OR A WORTHY CAUSE OR BOTH?

The majority of the respondents gave to both, a worthy cause and a church. Giving can have a powerful impact on you and the receiver(s)! It can do some of the following:

- Help the community

- Set an example for your children

- Gives a joyful feeling of doing something good

- Make you a little more compassionate

BASED ON WHAT YOU KNOW NOW ABOUT MONEY MANAGEMENT, WHAT ADVICE WOULD YOU HAVE GIVEN YOUR YOUNGER SELF YEARS AGO?

- Get on a budget and stick to it. Invest!!

- Get a good financial advisor

- Be sure to save money!

- Budget, save and invest

- Spend less & stay on a budget!

- Learn more about finances to include long-term saving

- Buy what you need, not what you want

WHAT ONE TIP YOU WOULD YOU GIVE FOR SAVING MONEY?

- Live by the 70/30 rule: 70% for expenses, 10% for tithing, 10% for saving, and 10% for investing

- Live below your mean

- Spend less than what you bring in

- Distinguish the difference between “needs” and “wants”

- Eat out less

- Take short local vacations

- Pack your lunch

This post is all about 30 financial management questions you should ask yourself that are designed to help you think more critically about your personal finance.

Other Post(s) and Resource(s) You May Like:

SEVEN (7) AMAZING SIMPLE TIPS FOR REDUCING YOUR PERSONAL FINANCIAL DEBT WHILE ACHIEVING PEACE AND BUILDING WEALTH

PERSONAL FINANCE| SIX (6) CATEGORIES YOU MUST UNDERSTAND TO BUILD A BETTER CREDIT SCORE

Recent Comments